- I am participating in RetirementPlus. What does this mean for my retirement benefit?

- I am not participating in RetirementPlus because I elected not to participate (or I didn’t submit a timely election form). Can I elect in now?

- How do I know if I am subject to RetirementPlus?

- How can I check my contribution rate?

- Why is the “9+2” regular contribution rate not the same as the 11% RetirementPlus contribution rate?

- How is the additional “plus” 2% on earnings over $30,000/year calculated?

- What happens if I am contributing or have contributed at “9+2,” but I should be at a flat 11% because I chose to participate in RetirementPlus?

- What is the difference in contributions for R+ if my rate is “8+2”?

![]() RetirementPlus update: Please check here for the latest news.

RetirementPlus update: Please check here for the latest news.

The RetirementPlus (R+) program increases retirement benefits for eligible and participating members who have completed 30 years of service (at least 20 of which are membership service with the MTRS or the Boston Retirement System as a teacher), and subject to the statutory maximum of 80 percent, as follows:

- for members with effective membership dates before April 2, 2012, an additional 2 percent for each full year of creditable service in excess of 24 years (e.g., at 30 years of creditable service, an additional 12%, or 6 years x 2%).

- for members with effective membership dates on or after April 2, 2012, an additional 2 percent for each full year of creditable service in excess of 23 years (e.g., at 30 years of service, an additional 14%, or 7 years x 2%).

The contribution rate for RetirementPlus participants is a flat 11%. See more information about contribution rates here.

RetirementPlus options for members who transfer to the MTRS from another Massachusetts public retirement system.

Participation in the R+ program is mandatory for all new members of the MTRS who have an account transfer into the MTRS on or after July 1, 2022, and whose prior service in another Massachusetts public retirement system began on or after July 1, 2022. Like all other teachers, these members have no election option and are required to participate in RetirementPlus.

Please refer to the table below for the impact to different member groups based on dates of membership and service.

| Your MTRS Membership Date | Date the MTRS receives the transfer of your account from the other Massachusetts public retirement system | RetirementPlus Election |

|---|---|---|

| Between 7/1/2001 and 6/30/2022 | Between 7/1/2001 and 6/30/2022 |

|

| On or after 7/1/2001 with service starting in the other MA public retirement system prior to 7/1/2022 | On or after 7/1/2022 |

|

| On or after 7/1/2022, with service starting in the other MA public retirement system on or after 7/1/2022 | On or after 7/1/2022 |

|

For tables showing the percentages of salary average allowed by age, years of service and formula (regular or RetirementPlus), please see “Retirement percentage” charts.

Background

Original election of 2001

In February 2001, then-current members of the MTRS were mailed an Election Form and given until June 30, 2001 to affirmatively elect to participate in RetirementPlus. Members who did not return their election form were not included in RetirementPlus.

Special election of 2023

On August 3, 2022, then Governor Charlie Baker signed into law Chapter 134 of the Acts of 2022 which–among other changes to how RetirementPlus is implemented for MTRS members–allowed for members who had 1) transferred-in service between July 1 2001 and June 30, 2022 and 2) never responded to their original RetirementPlus participation decision a new special election opportunity period which ran from January 1 to June 30, 2023. The special election period has now come to a close.

Inactive members of the MTRS must still make an election

In any scenario, if you become an inactive member of the MTRS and are provided with an opportunity to participate or not participate in RetirementPlus, you must still make this election and submit your decision to the MTRS.

We realize you may no longer be teaching in Massachusetts; however, it is important to act on your election because it will determine your contribution rate if you return as an active member of the MTRS or Boston Retirement Board.

Please log in to your MyTRS account to update any changes to your mailing address, email address, and phone number.

FAQs

I am participating in RetirementPlus. What does this mean for my retirement benefit?

If you are participating in RetirementPlus—because you either elected to participate or you became a member of the MTRS on or after July 1, 2001—you will be eligible to receive a RetirementPlus enhanced benefit if, at the time of your retirement, you:

- have accrued 30 or more years of creditable service, at least 20 of which are membership service with the MTRS or the Boston Retirement System as a teacher, and,

- have contributed at the RetirementPlus rate of 11% for at least five years, or have made accelerated payments to meet this contribution requirement.

However, if you are participating in RetirementPlus because you elected to participate in RetirementPlus, and you:

- do not accumulate 30 years of creditable service by your date of retirement, you will receive a retirement benefit calculated under the regular formula, and a refund of your RetirementPlus contributions, plus regular interest.

- retire with 30 or more years of creditable service, but fewer than 20 of your years are as a member of the MTRS or the Boston Retirement System as a teacher, you will receive the regular retirement benefit and a refund of your RetirementPlus contributions, plus regular interest.

Please note that if you are participating in RetirementPlus because you became a member of the MTRS on or after July 1, 2001, and you do not meet the criteria to be eligible for the enhanced RetirementPlus benefit, you are not entitled to a refund as your contribution rate of 11% was mandatory.

I am not participating in RetirementPlus because I elected not to participate (or I didn’t submit a timely election form). Can I elect in now?

For the majority of members, the answer is “No”; your election opportunity was a one-time chance. If you did not elect to participate, you cannot later opt in. If, however, you leave MTRS service, take a refund of your annuity savings account and then return to MTRS service, you will return as a new member and automatically be subject to RetirementPlus and the contribution rate of 11%. The only exception was for members who were not a part of the original election window prior to July 1, 2001, and transferred into the MTRS from one of the other 103 Massachusetts public retirement systems between July 1, 2001 and June 30, 2022, and did not yet submit an election. These eligible members had a final, one-time opportunity to participate between January 1, 2023 and June 30, 2023.

How do I know if I am subject to RetirementPlus?

If you:

- Transferred to the MTRS from another Massachusetts contributory retirement system:

- Prior to July 1, 2022 – transferred to the MTRS from another Massachusetts contributory retirement system on or after July 1, 2001, you had 180 days from the date that you transferred into the MTRS to enroll in RetirementPlus. If you submitted an affirmative election within 180 days, you are subject to RetirementPlus.

- After July 1, 2022 – transferred to the MTRS from another Massachusetts contributory retirement system on or after July 1, 2022, you have 180 days from the date that you transferred into the MTRS to opt-out of RetirementPlus. If you do not submit an election choice within 180 days, you will be subject to RetirementPlus.

- joined the MTRS as a new member to a Massachusetts public retirement system on or after July 1, 2001, you are automatically enrolled in RetirementPlus.

- were a member of the MTRS prior to July 1, 2001, you had until June 30, 2001 to elect to participate in RetirementPlus. If you did not submit a timely, affirmative election, you were not enrolled in RetirementPlus and your contribution rate remained the same.

How can I check my contribution rate?

Look at your pay stub. Divide the amount of your retirement withholding by your gross income, and then refer to the contribution chart. For example, if your enrollment date is January 2, 1979 and your salary is $35,000, your total contribution would be 7% of $35,000 plus 2% of $5,000. The 2% contribution does not apply to RetirementPlus participants.

If your contribution rate is not correct, confirm your calculation with your payroll office and then contact the MTRS. Note: If the 2% contribution also applies, be sure it appears on your pay stub.

For more info, watch this section of our RetirementPlus special election seminar, recorded on 02/23/2023 (link will open in YouTube, watch only 14:45-20:45).

Why is the “9+2” regular contribution rate not the same as the 11% RetirementPlus contribution rate?

If you are not participating in RetirementPlus, you are contributing at one of the lower contribution rates within the grid above—most likely the 9% flat rate on your entire salary, with an additional 2% on earnings over $30,000. This rate is called “9+2” or “9 and 2.” Pay stubs may also label these additional 2% contributions as “RET2,” “ADDL2%,” “PLUS2,” or some variation of these examples. Some members may also hear or see the word “plus” and believe this means RetirementPlus.

The differences between these two rates can be confusing because the lower “9+2” rate is a common rate established at other Massachusetts contributory retirement systems, one could assume that 9% plus 2% on earnings over $30,000/year adds up to a flat 11%, but that is not the case. It is important to remember that the additional 2% withholding is only on a portion of your salary, not the entire amount.

For example: Joe Teacher recently transferred into the MTRS from another Massachusetts contributory retirement system.

R+ Flat 11% Contribution Rate

If Joe decides to participate in R+, his bi-weekly contribution would be:

$2,230.77 x 11% = $245.38

“9+2” Contribution Rate

If Joe decides to opt out of R+, his bi-weekly contribution would be:

$2,230.77 x 9% = $200.77

2% contributions on earnings over $30,000: $21.54$200.77 + $21.54 = $222.31 (total “9+2”)

The difference between both contribution rates is $23.07 ($245.38 – $222.31). The annual difference is $600 ($23.07 x 26). The difference per paycheck will vary depending on the number of paychecks you receive in a year; however, the annual difference between 11% and “9+2” will always be $600/year, unless something abnormal occurs with your pay or you make less than $30,000 in one calendar year.

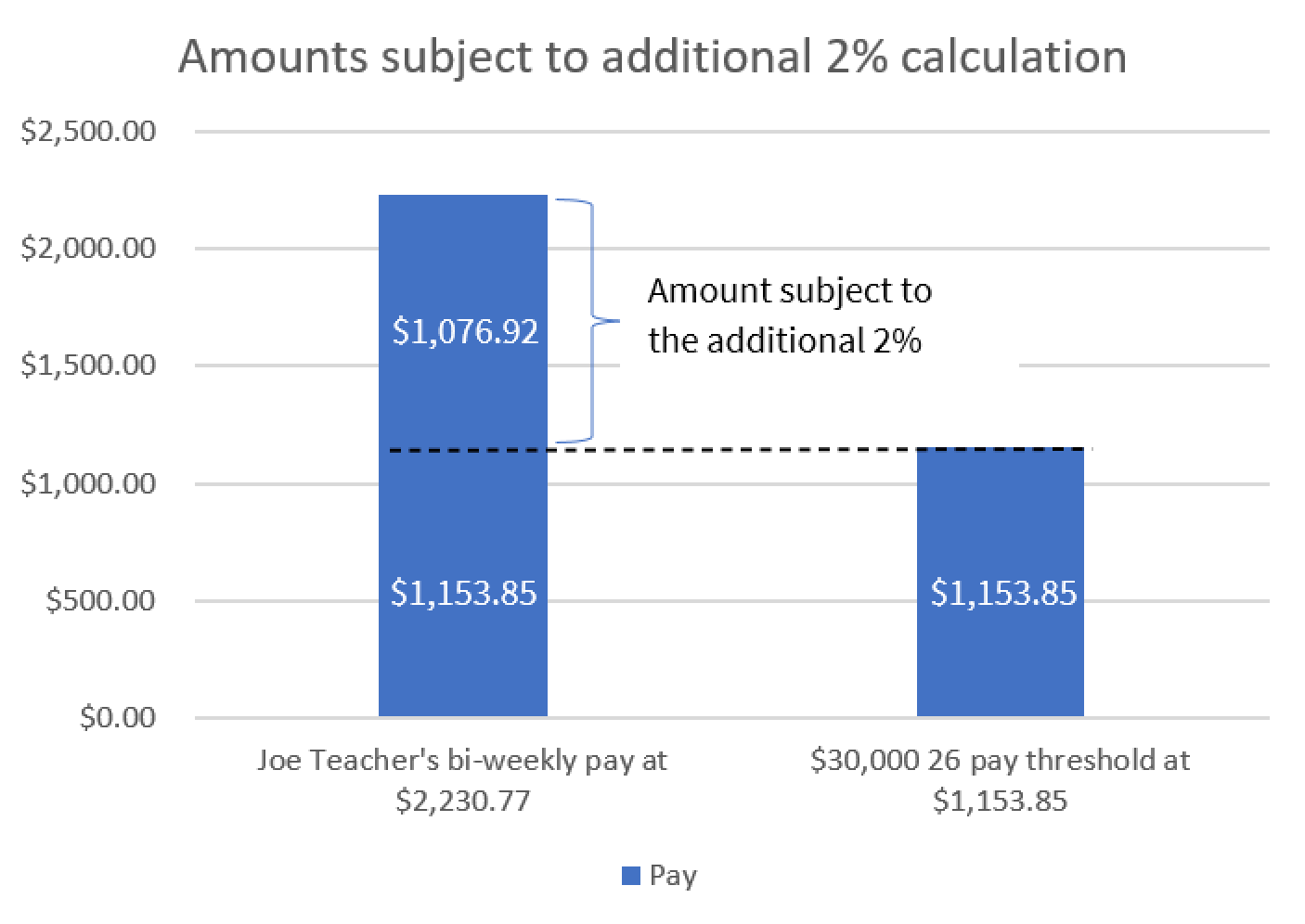

How is the additional “plus” 2% on earnings over $30,000/year calculated?

According to PERAC memo #43 from 1999, the additional 2% must be calculated on a per pay period basis. Rather than subtracting $30,000 from your entire salary, it must be done incrementally from each pay throughout the year.

First, you must figure out the number of times you are paid each year. Many members receive their pay over 26 pay periods; therefore, we will use this in our calculation example.

If Joe Teacher makes $58,000 per school year and is paid bi-weekly over 26 pays, his gross bi-weekly pay is $2,230.77, the portion of which “above” $30,000 is $1,076.92 ($30,000/26=$1,153.85; $2,230.77-$1,153.85=$1,076.92)

The 2% is then withheld from $1,076.92. Joe’s 2% contribution is $21.54 ($1,076.92 x 2%).

For more information on the difference between 11% and 9%+2% contribution rates, watch this section of our RetirementPlus special election seminar, recorded on 02/23/2023 (link will open in YouTube).

What happens if I am contributing or have contributed at “9+2,” but I should be at a flat 11% because I chose to participate in RetirementPlus?

If you elected to participate in RetirementPlus and your school district is currently withholding at a rate lower than 11%, your rate will need to be changed immediately. As a reminder, someone who chooses to participate in RetirementPlus will owe the difference between 11% and any lower rate. All shortages in your account, going back to your MTRS membership date, must be paid to make your account whole.

You will eventually receive these contributions back as part of your future retirement benefit; however, it is important for the system to invest these funds to provide you and all our members with a lifetime benefit.

What is the difference in contributions for R+ if my rate is “8+2”?

If your contribution rate is an 8% flat rate on your entire salary, with an additional 2% on earnings over $30,000, often referred to as “8+2”, the difference between 11% and 8+2 is significantly higher. For illustrative purposes, the chart below lists annual costs for average wages in $10,000 increments.

“8%+2%”

You will pay 11% on all of your future wages, and your retroactive cost will depend on your wages during your prior MTRS service. For illustrative purposes, the chart below lists annual costs for average wages in $10,000 increments:

For example*: If your Contribution Rate since you joined the MTRS is 8% + 2% And your average salary during your MTRS membership was: Then, for each year you have been a member of the MTRS, you will owe: $40,000 $1,000/year $50,000 $1,100/year $60,000 $1,200/year $70,000 $1,300/year $80,000 $1,400/year $90,000 $1,500/year $100,000 $1,600/year $110,000 $1,700/year $120,000 $1,800/year

For example*: Sarah Teacher has 10 years of prior MTRS service and her average wages during that service were $70,000, thus, her retroactive cost would be $13,000 ($1,300/yr x 10 years = $13,000).

*These examples are for illustrative purposes only.